42 what is the duration of a zero coupon bond

What is a zero bond? - Foley for Senate The duration of a zero coupon bond is equal to its maturity. Duration is a weighted average of the maturities of all the income streams of a bond or a portfolio of bonds. Therefore if there are coupons, the duration will be less than the maturity, and if there are no coupons it will be equal to its maturity. Duration of zero coupon bond - Fixed Income - AnalystForum Oct 10, 2007 — The weight used for each cash flow is its present value divided by the total present value of the bond. In the very simple case of a zero coupon ...

Zero Coupon Bond | Investor.gov The maturity dates on zero coupon bonds are usually long-term—many don't mature for ten, fifteen, or more years. These long-term maturity dates allow an investor to plan for a long-range goal, such as paying for a child's college education. With the deep discount, an investor can put up a small amount of money that can grow over many years.

What is the duration of a zero coupon bond

Zero-Coupon Bond: Formula and Excel Calculator Generally, zero-coupon bonds have maturities of around 10+ years, which is why a substantial portion of the investor base has longer-term expected holding periods. Solved a. What is the duration of a zero-coupon bond that | Chegg.com a. What is the duration of a zero-coupon bond that has six years to maturity? Duration of the bond= _____ years. b. What is the duration if the maturity increases to 7 years? Zero-coupon bond - Wikipedia A zero coupon bond always has a duration equal to its maturity, and a coupon bond always has a lower duration. Strip bonds are normally available from investment dealers maturing at terms up to 30 years. For some Canadian bonds, the maturity may be over 90 years.

What is the duration of a zero coupon bond. The One-Minute Guide to Zero Coupon Bonds | FINRA.org After 20 years, the issuer of the bond pays you $10,000. For this reason, zero-coupon bonds are often purchased to meet a future expense such as college costs or an anticipated expenditure in retirement. Federal agencies, municipalities, financial institutions and corporations issue zero-coupon bonds. The Macaulay Duration of a Zero-Coupon Bond in Excel The Macaulay duration of a zero-coupon bond is equal to the time to maturity of the bond. Simply put, it is a type of fixed-income security that does not pay interest on the principal amount. Zero-Coupon Bonds: Pros and Cons - Management Study Guide Zero-coupon bonds are commonly issued by governments. In this article, we will have a closer look at the pros and cons of zero-coupon bonds from an investor's point of view: Pros of Zero-Coupon Bonds. There are many zero-coupon bonds that are already in existence. Also, each year, many new zero-coupon bonds are issued. What is the duration of a zero coupon bond? - Quora Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with par value paid on redemption, sometimes with a nominal premium.

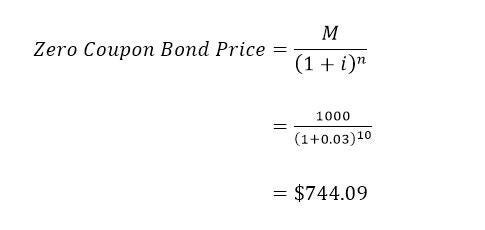

Zero-Coupon Bond - Definition, How It Works, Formula Example of a Zero-Coupon Bonds Example 1: Annual Compounding. John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? 5 = $783.53. The price that John will pay for the bond today is $783.53. 61what is the duration of a 10 year zero coupon bond 61.What is the duration of a 10 year zero coupon bond. Assume the bond is callable (ie, the issuer can buy it back) at face value at any time during its existence. A. 0 years B. 5 years C. 1 year D. 10 years Answer: D Explanation: The key point in this question is that the bond is zero coupon, and can only be called at face value. Since the bond is zero coupon, its value will always be less ... Duration of a callable zero bond | Forum | Bionic Turtle Consider a $100 face value 10-year zero-coupon bond that is callable (European-style) in one year at 80 percent of its face value. Figure 2.2 plots the bond's price, duration, and dollar duration as a function of yield. The bond price as a function of yield first steepens, and then flattens as yield increases (see Figure 2.2 What Is a Zero-Coupon Bond? Definition, Characteristics & Example This means that they must pay taxes on income they will not receive until their bond matures. For instance, if a zero-coupon bond was sold at a $100 discount and matures in four years, its holder ...

Understanding Zero Coupon Bonds - Part One - The Balance Here is an example of how zero coupon bond prices can change: For example, assume that three STRIPS are quoted in the market at a yield of 6.50%. As you can see, the farther out you go the lower your front-end cost and the more work compounding does to get you to the full face value. Solved a. What is the duration of a zero-coupon bond that - Chegg a. Duration of the bond b. Duration of the bond c. Duration of the bond years years years. Question: a. What is the duration of a zero-coupon bond that has eight years to maturity? b. What is the duration if the maturity increases to 10 years? c. Dollar Duration - Overview, Bond Risks, and Formulas Dollar duration can be applied to any fixed income products, including forwarding contracts, zero-coupon bonds, etc. Therefore, it can also be used to calculate the risk associated with such products. Summary Dollar duration is the measure of the change in the price of a bond for every 100 bps (basis points) of change in interest rates. Solved What is the duration of a zero coupon bond with a YTM | Chegg.com What is the duration of a zero coupon bond with a YTM of 4% and a maturity of 10 years? Who are the experts? Experts are tested by Chegg as specialists in their subject area. We review their content and use your feedback to keep the quality high. In zero coupon Bond there are no intermediate payment in the form of coupon payment for interest ...

Advanced Bond Concepts: Bond Pricing | Investopedia

Zero Coupon Bond | Definition, Formula & Examples - Study.com A zero-coupon bond still has 5 years to mature and is currently priced at $760 in the capital market. Assume that the face value is $1,000 and the required interest rate of the bond is 5%...

Use Duration And Convexity To Measure Bond Risk

Zero Coupon Bond (Definition, Formula, Examples, Calculations) Duration: The duration of a Zero-coupon Bond is equal to the maturity of the Bond. The duration of the Regular bond will always be less than its maturity. Interest Rate Risk

Zero Coupon Bonds - YouTube

Zero Coupon Bond Calculator - What is the Market Price? - DQYDJ Duration of a bond is a length of time representing how sensitive a bond is to changes in interest rates. Since zero coupon bonds have an equal duration and maturity, interest rate changes have more effect on zero coupon bonds than regular bonds maturity at the same time. (Whether that's good or bad is up to you!)

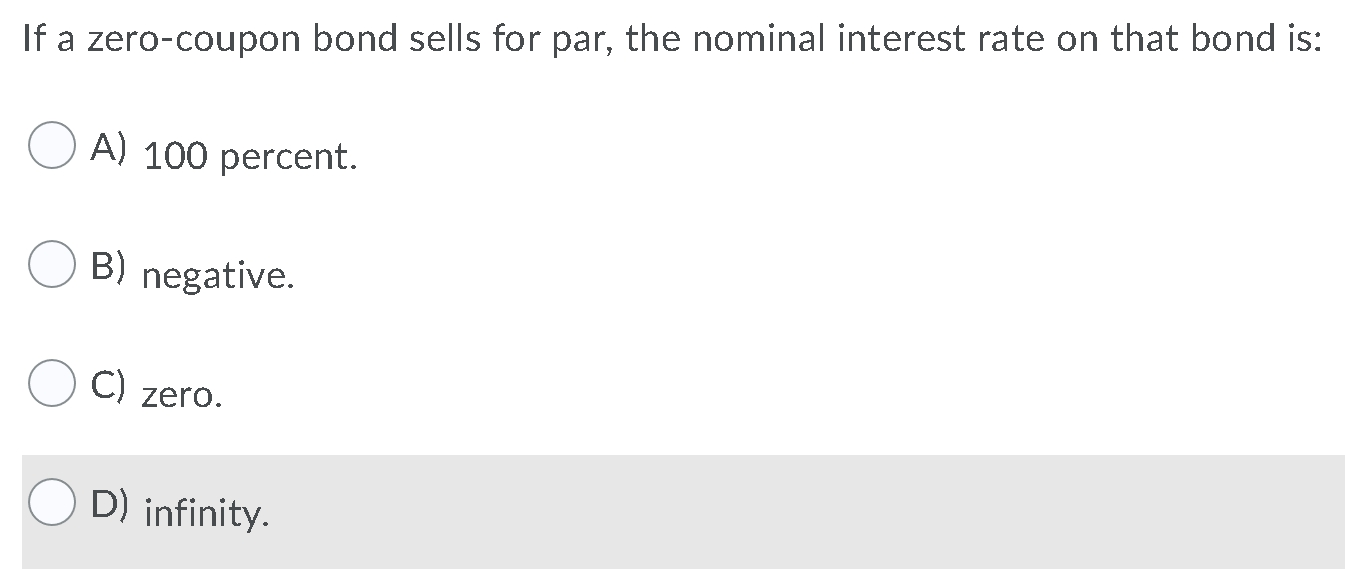

Solved: If A Zero-coupon Bond Sells For Par, The Nominal I... | Chegg.com

How Do Zero Coupon Bonds Work? - SmartAsset What Is a Zero Coupon Bond? A zero coupon bond is a type of bond that trades at a deep discount and doesn't pay interest. While some bonds start out as zero coupon bonds, others are can get transformed into them if a financial institution removes their coupons. When the bond reaches maturity, you'll get the par value (or face value) of the ...

Bond valuation

Zero Coupon Bond Value - Formula (with Calculator) A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value.

Bond pricing - Bogleheads

Zero-Coupon Bond Definition - Investopedia The maturity dates on zero-coupon bonds are usually long-term, with initial maturities of at least 10 years. These long-term maturity dates let investors plan for long-range goals, such as saving...

Post a Comment for "42 what is the duration of a zero coupon bond"